03.2022 Life Guide

A new choice in the era of low interest -- "interest offsetting housing loan" offsetting housing loan with deposit

Far Eastern International Bank / Wu Ruimin

Since the second half of 2021, the growth rate of inflation in Taiwan has risen to 2.62%, far exceeding the deposit interest. At this time, the "interest mortgage" that can retain more cash positions may be a new choice in the era of low interest.

Since the second half of 2021, the growth rate of inflation in Taiwan has risen to 2.62%, far exceeding the deposit interest. At this time, the "interest mortgage" that can retain more cash positions may be a new choice in the era of low interest.1、 What is interest mortgage?

As the name suggests, "interest offset housing loan" means that the balance of living savings deposit and housing loan are offset against each other. The interest offset is used to reduce the monthly payment or accelerate the repayment of principal, and maintain the flexible use of the position of living savings deposit. At present, there are mainly two discount methods in the market:

1. Interest offset (change in monthly payment): after the balance of the principal of the mortgage is offset against the balance of the deposit, the saved interest is offset against the current interest expense.

2. Principal offset (fixed monthly payment): after the balance of the principal of the mortgage is offset against the balance of the deposit, the saved interest is offset against the beginning principal of the next period.

For example, Mr. Wang likes to keep more cash positions, so he applies for a 20-year mortgage of 10 million yuan, with an interest rate of 2%, and deposits 1 million yuan into the deposit account of the mortgage. Then the bank only calculates the interest of the principal balance of 9 million yuan (10 million yuan – 1 million yuan = 9 million yuan), of which the mortgage of 1 million yuan is free of interest.

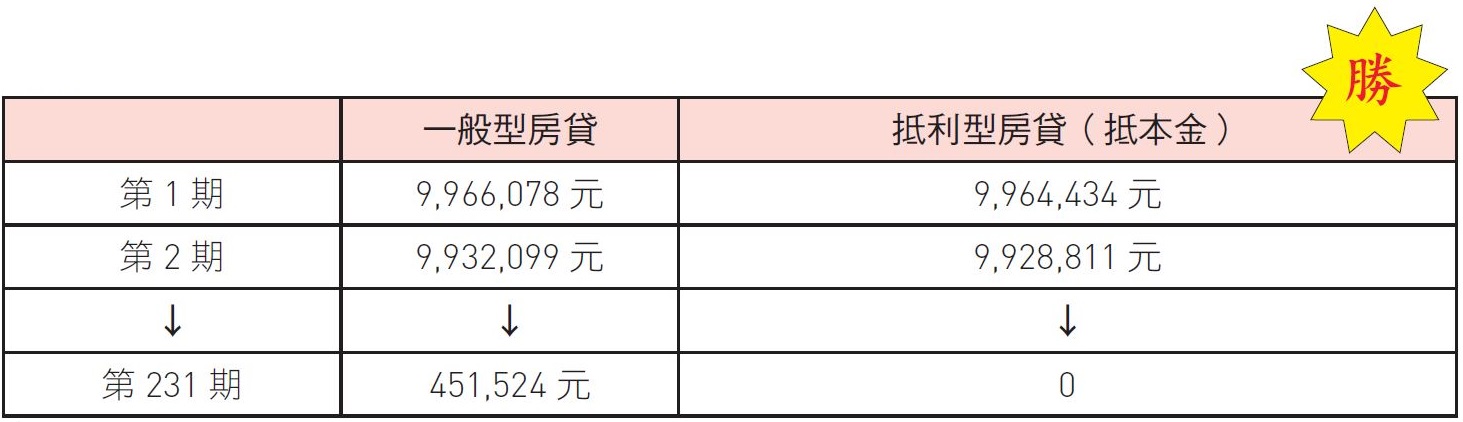

The original 20-year general mortgage monthly payment was 50589 yuan. If Mr. Wang chooses to apply for the interest deduction mortgage (monthly payment change), the interest can be converted into 1644 yuan (1 million yuan) based on the 30 days of the current month × 2% ÷ 365 days × 30 days = 1644 yuan), in other words, the monthly payment is reduced from 50589 yuan to 48945 yuan (50589 yuan - 1644 yuan = 48945 yuan). The monthly payment is reduced and the payment is easier.

On the other hand, if Mr. Wang chooses to apply for the interest mortgage with the principal offset (fixed monthly payment), the principal can be converted into 1644 yuan (1 million yuan) based on the same 30 days of the current month × 2% ÷ 365 days × 30 days = 1644 yuan), compared with ordinary housing loans, the principal balance is reduced by 1644 yuan, accelerating the decline of principal, shortening the repayment period and settling the loan before the maturity date of the housing loan.

On the other hand, if Mr. Wang chooses to apply for the interest mortgage with the principal offset (fixed monthly payment), the principal can be converted into 1644 yuan (1 million yuan) based on the same 30 days of the current month × 2% ÷ 365 days × 30 days = 1644 yuan), compared with ordinary housing loans, the principal balance is reduced by 1644 yuan, accelerating the decline of principal, shortening the repayment period and settling the loan before the maturity date of the housing loan. 2、 What are the advantages of mortgage products?

2、 What are the advantages of mortgage products?1. Deposit interest can be converted into mortgage interest to reduce loan expenditure

The amount deposited into the deposit account of interest offset housing loan can be converted into the balance of housing loan, and the deposit interest rate is equivalent to the interest rate of housing loan; In the current low interest environment, it has a more spread effect. The more the deposit amount, the more interest will be saved.

In Mr. Wang's case mentioned above, if 1 million yuan is deposited into the deposit account of interest offset (principal offset) housing loan at one time, the loan expenditure can be reduced by 460000 yuan compared with ordinary housing loan; If 2 million yuan is deposited, the loan expenditure of 860000 yuan will be reduced, and so on.

2. Shorten the loan period

If you choose to offset the interest type housing loan (offset the principal), you can also shorten the repayment period and repay the loan in advance. For example, if Mr. Wang deposits 1 million yuan, the loan period can be shortened to 19 years and 3 months; If the deposit is 2 million yuan, the loan period will be shortened to 18 years and 7 months.

3. Deposit funds can be used flexibly

When there is a temporary demand for funds, you can also use the deposit account at any time to retain the flexibility of fund utilization, and there is no need to apply for additional loans or credit loans.

3、 Precautions for applying for interest mortgage

1. There is a difference in the upper limit of interest deduction for mortgage loans of various banks

In addition to the functional difference of offsetting principal or interest, there are also differences in the upper limit of discount. At present, the upper limit of discount on the market is divided into 100%, 70%, 50% and 30% respectively. Except for the products with the upper limit of 100%, if the amount of other deposits exceeds the upper limit of loan balance, it will not have the effect of offsetting interest. Taking the loan balance of 10 million yuan as an example, when the upper limit of discount is 30%, the maximum amount of deposit can only be converted into the loan of 3 million yuan; Therefore, when the deposit amount is 4 million yuan, of which 1 million yuan cannot be offset.

2. The interest rate of interest offset housing loan is higher than that of general housing loan

Because the bank does not charge the interest on the part of the deposit converted into the mortgage, in order to pay the internal operation cost of the bank, the interest rate is usually higher than that of the general mortgage, and the higher the upper limit of the discount, the higher the mortgage interest rate. At present, the general interest rate of the self occupied mortgage in the market is about 1.35% 1.5%, and the interest rate of the interest offset mortgage is about 1.5% 2.0%.

3. The live savings account does not bear interest

As a credit account, the deposit account of mortgage loan with interest offset is not subject to deposit interest regardless of the amount of deposit. Taking the loan balance of 10 million yuan as an example, when the upper limit of discount is 30%, the deposit amount can only be converted into the loan of 3 million yuan at most. Therefore, when the deposit amount is 4 million yuan, more than 1 million yuan can not be converted and there will be no deposit interest.

4. Deduction of loan interest affecting house purchase

According to the tax law, the interest paid on the purchase of self used residential loans shall be deducted by 300000 yuan per household every year. If the special deduction for savings and investment is reported at the same time, it shall be deducted from the interest on the purchase of housing loans. Although the deposit account linked with the mortgage interest can offset the mortgage interest, the part of the deposit interest offset belongs to "interest income" and still needs to be incorporated into the comprehensive income tax of the current year.

For example, the total interest expense of housing loan in the current year is 200000 yuan and the fixed deposit interest income is 16000 yuan. If you apply for a general housing loan, the deduction of interest expense of house purchase loan can be listed as 184000 yuan. (200000 yuan - 16000 yuan = 184000 yuan)

If you apply for an interest offset housing loan, because the income after deducting the interest is 40000 yuan, the deduction of interest expense of house purchase loan can be listed as 160000 yuan. (200000 yuan - 40000 yuan = 160000).

5. The supplementary premium of health insurance may be increased

The interest offset loan belongs to "interest income" because the discount of the deposit account still belongs to the interest specified in Article 14 of the income tax law, and the bank must also open a withholding voucher for the interest of the deposit account, so it is the scope of supplementary insurance premium calculation and collection; If the single payment amount reaches 20000 yuan, the supplementary insurance premium shall be calculated and charged. But in fact, at the interest rate of 1.9%, the supplementary premium will not be generated until the deposit exceeds $12.2 million.

6. Charge

General housing loans usually charge start-up fees, and liquidated damages will also be charged for early repayment of loans. Similarly, for interest offset housing loans, banks may have different amounts and regulations, which should be understood before bidding.

If you want to keep a sum of cash around you or have the habit of saving, in the low interest environment, you might as well choose the interest offset housing loan. Although the interest rate is high, you can keep cash as the living reserve fund, investment and financial management, working capital for small-scale dealer operation, etc., which can also reduce the loan expenditure and repay the loan in advance. However, it is suggested to compare the upper limit of interest deduction and interest rate level of several banks, consider their own deposit amount and choose the most suitable scheme.

#