08.2022 Life Guide

The interest rate hike is officially launched, you need to make money big

Far Eastern International Bank / Chen Mengli

After Taiwan launched the first wave of interest rate hikes in March, the fixed deposit rate returned to the first digit again. How should you adjust your asset allocation at this time to increase your wealth?

After Taiwan launched the first wave of interest rate hikes in March, the fixed deposit rate returned to the first digit again. How should you adjust your asset allocation at this time to increase your wealth?When will the "rate hike"?

When economic growth slows, the central bank may adopt “interest rate cuts” to promote economic development; when the economy is back on track, it will adopt “interest rate hikes” to bring interest rates back to normal levels and avoid overheating inflation. In the event of an event with a greater impact on the economy, the central bank is more likely to cut interest rates sharply to save the economy. In fact, the cyclical process from cutting interest rates to raising interest rates has happened countless times in history, such as the "tech bubble" in 2000, the "financial tsunami" in 2008, and the recent "COVID-19" epidemic. (see Table 1).

After the outbreak of the epidemic in 2020, the US Federal Reserve System (Fed) cut interest rates by 6 yards in just one month, from 1.5-1.75% to 0-0.25%. Central banks also urgently followed up, and Taiwan's central bank also cut interest rates by one percent. The world has officially entered the "zero interest rate era". After two years, the epidemic has gradually cleared up, and inflation has continued to rise. The US Federal Reserve System raised interest rates by one yard in March 2022, officially starting the cycle of interest rate hikes to curb inflation and stabilize the economy, and then raised interest rates in May. 2 yards, in June, it raised interest rates 3 yards in one go, and the Central Bank of Taiwan also raised interest rates by 1 yards in March and half a yard in June.

After the outbreak of the epidemic in 2020, the US Federal Reserve System (Fed) cut interest rates by 6 yards in just one month, from 1.5-1.75% to 0-0.25%. Central banks also urgently followed up, and Taiwan's central bank also cut interest rates by one percent. The world has officially entered the "zero interest rate era". After two years, the epidemic has gradually cleared up, and inflation has continued to rise. The US Federal Reserve System raised interest rates by one yard in March 2022, officially starting the cycle of interest rate hikes to curb inflation and stabilize the economy, and then raised interest rates in May. 2 yards, in June, it raised interest rates 3 yards in one go, and the Central Bank of Taiwan also raised interest rates by 1 yards in March and half a yard in June.Interest rate hike vs. deposit allocation advice

Affected by the interest rate hike by the Central Bank of Taiwan, various banks have also raised their interest rates. Taking Far Eastern International Bank as an example, the "one-year fixed savings" fixed interest rate was about 0.79% before the rate hike, and after the rate hike in March It was raised to 1.06%, an increase of 0.27%; after the interest rate hike in June, it was raised to 1.225%, an increase of 0.165%. In other words, if you deposit NTD1,000,000 in the "one-year fixed deposit", the annual interest will change from NTD7,900 to NTD12,250, which is equivalent to an annual increase of NTD4,350 in interest. But if the time goes back to last year and the same asset allocation is adopted when the interest rate is cut, the interest will be reduced by NTD4,350 per year. It can be seen from this that when interest rates are raised, the allocation of deposit positions can be increased; when interest rates are lowered, adjustments should be made to accumulate wealth flexibly.

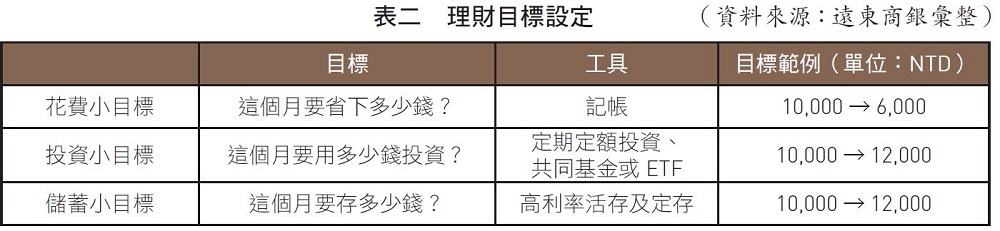

Set basic asset allocation Set personal goals

If you want to accumulate wealth quickly, you must first have basic asset allocation. The easiest way is to divide monthly income into “savings”, “investments” and “expenses”, where “savings” refers to demand deposits or time deposits deposited in banks; “investments” include stocks, funds and other commodities; "Expense" refers to the consumption of food, clothing, housing, transportation, education, and entertainment. Next, as long as you grasp the concept of "saving + investment - spending = increased wealth" and set personal goals, you can further implement financial planning.

Assume that the monthly salary is NTD30,000, and evenly distribute NTD10,000 among "savings", "investments" and "expenses", and then set a "spending small target" to decide how much to save this month. If you don't know where your salary is going, it is recommended to use an accounting tool for assistance. Assuming that the "small spending target" is reduced from NTD10,000 last month to NTD6,000, it means that spending on leisure and entertainment needs to be moderated, or the frequency of eating large meals can be reduced. If you can successfully save NTD4, 000, which can be allocated to the small goals of "Investment" and "Savings". Among them, the "small investment goal" does not depend on how much money you earn by investing. After all, investing may not be profitable every day. You might as well make good use of financial tools to invest in mutual funds or ETFs on a regular basis to achieve average cost and accumulation. In addition, compared with investment, the risk of bank savings is very low. You can consider putting your funds in high-interest demand or time deposit commodities, or you can choose long-term time deposits. On the one hand, you can get more High interest, on the other hand, can force yourself to save money, and over time, you can accumulate the first pot of gold in life. (Detailed table 2)

Grasp the rate hike and earn interest

In the environment of rising interest rates, in addition to keeping some funds alive and using them at any time, it is also recommended to increase the allocation to fixed deposits. Whether New Taiwan dollar or foreign currency fixed deposits are good choices, especially with the interest rate hike in the United States this year, various A bank has also launched a USD time deposit project with an attractive interest rate. If you have already exchanged some more USD while the exchange rate was cheap in the past two years, you might as well put it in USD time deposit first, as a future travel fund or an education fund for your children to study abroad. .

#